|

In fact, the World Economic Forum recently ranked Australia as the second among the world's financial centres, behind only the United Kingdom, primarily due to the stability of our financial institutions over the past 12 months. The tax treatment of Islamic financial products should be based on their economic substance rather than their form. Fees and charges may apply, as well as terms and conditions which you should review. In order to open a credit product in future, you will need to meet our credit criteria and be approved. Please review the product disclosure documentation provided at the time of opening your account for detailed information. "I'm very grateful that this is allowing me to grow my business," he says. "A lot of people that we know that are Muslims have gone with conventional ways." "We made a whole series of suggestions for the government to apply that got lost," he says. The complication in the Australian context is that laws aren't set up for this style of lending, so technically the home is owned by the household from the beginning, but with a legal agreement that the Islamic lender is entitled to it. Designed to meet Islamic Law requirements, the product structures financing as a lease where ‘rent’ and ‘service fee’ are paid instead of ‘interest’. The Bank has also invested in achieving the endorsement of Amanie Advisors, a global Shariah advisory firm on behalf of its customers to provide comfort around the law compliancy while saving clients valuable time and money. However, according to Ernst & Young, Islamic banking assets have experienced rapid growth and are forecast to increase by an average of 19.7% a year until 2018. A number of Australian financial institutions have examined Muslim financing concepts such as profit sharing and rent to buy while trying to avoid terms such as "interest" in contractual agreements. Islamic home loans are available for many purposes such as construction and purchasing vacant land, although they are not typically used for refinancing. They also come in full documentation and low documentation versions, depending on your leasing needs. Speaking to The Adviser on the occasion of the RADI being granted, Islamic Bank Australia chief executive Dean Gillespie outlined that the bank will look to distribute home finance through the broker channel, as well as direct. Settle Easy has updated its online platform to provide automatic updates to mortgage brokers and real estate agents during the conveyancing ... National Australia Bank today announced that it has invoked its disaster relief package for customers impacted by bushfires in the Perth Hills area of Western Australia. This service may include material from Agence France-Presse , APTN, Reuters, AAP, CNN and the BBC World Service which is copyright and cannot be reproduced. On the question of signing up to an Islamic bank with deposit account capabilities, Melbourne couple Melike and Ibrahim had mixed views. Sydney-based startup IBA Group, which is led by Muslim scholars, told ABC News they started the process with APRA to get a R-ADI a few years ago. For example, the bank might buy a $10,000 car and sell it to the customer for $13,000 – which can be repaid in instalments. Whether because of, or despite, the global financial crisis, the need for greater accommodation of Islamic finance as a positive influence on our economy is being recognised by companies here and potential partners overseas. An opportunity for Australia to benefit from its advantages is in the funds management sector. Australia has expertise, experience and a well recognised reputation worldwide in funds management; diversifying the sources of debt finance. In addition, the Government has established a cross agency interdepartmental process to examine whether there are any non-tax regulatory barriers to the development of Islamic finance in Australia. My trip to the Middle East illustrated the vibrancy and dynamism of the Islamic finance sector and identified opportunities for Australia and the Middle East to work together in matters involving Islamic finance. We’re working as fast as we can to achieve our full ADI licence and bring our products to the Islamic community and all Australians,” Mr Gillespie said. The report concluded Australia has arguably the most efficient and competitive financial sector in the Asia-Pacific region, but there are further opportunities to expand our exports and imports of financial services. Australia is highly regarded internationally as a place to do business. Saving People from Riba Home loan applications continue to decline, according to the latest Equifax data. Without this approach, the gap on financial inclusion will only widen or contribute to diminishing financial health. IBA's licence is timely too, with the 2021 Australian Census highlighting a 34.6 per cent increase in Australia’s Islamic population — now the second largest religion in our country. We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision. "We've recognised that the Islamic finance industry has grown at a rate of about 15 per cent since the 1990s," NAB's director of Islamic finance, Imran Lum, tells ABC News. But in the past decade, he has been taking out more Islamic loans, including one just a few months ago to expand his company's meat-processing ability. Yet, despite making an Australian gastronomic icon, over the years the small business owner has felt excluded from the country's financial system and investment opportunities. The couple also intentionally avoids mainstream interest-based loans. When Halal Finance In Australia they wanted to buy a new car, they saved up and bought it outright. The complication in the Australian context is that laws aren't set up for this style of lending, so technically the home is owned by the household from the beginning, but with a legal agreement that the Islamic lender is entitled to it. There are no significant commercial benefits or features of Islamic home loans that wouldn’t be offered with a non-Islamic-compliant loan. “Islamic finance is largely about the philosophical side of things – it’s where Western banking meets Islamic banking. We offer an alternative solution for Muslims in an Australian landscape. Islamic finance is underpinned by Sharia values that are consistent with Islamic legislation. The fundamental principles concerned with Islamic home loans are outlined below. As general manager of Iskan Finance, Russell Murphy states, “For our customers, at the date of settlement, they are registered as the owner. For security reasons please DO NOT provide any confidential or account specific information via email. Communications via email that are not encrypted are not secure. What you need to know as an MCCA customer, or more generally as a member of Australia’s Muslim community or the finance profession. System is currently experiencing issues and we are working on a solution. Target Market Determinations can be found on the provider's website. For more information please see Mozo's FSG, General advice disclaimer or Terms of use. Islamic Bank Australia (islamicbank.au) will be the first Australian bank to offer a full suite of retail and business banking services – all without interest and Shariah-compliant for the first time in Australia. The bank will first launch retail/personal banking with an everyday bank account, savings product (accounts that pay profit-share) and home finance (with co-ownership), before moving into business banking after a full licence is received. But, inclusion isn’t just about access, it’s also about experience. Australias first Islamic Bank set to open soon Learn more about Islamic home loans, including how they work and what to look for. You can also compare other home loans and get a better idea of their costs and benefits. Canstar is a comparison website, not a product issuer, so it’s important to check any product information directly with the provider. Consider the Product Disclosure Statement , Target Market Determination and other applicable product documentation before making a decision to purchase, acquire, invest in or apply for a financial or credit product. Contact the product issuer directly for a copy of the PDS, TMD and other documentation. If you’re Muslim, then you may have wondered for a long time about how you can get a mortgage so you can own your own home and stay true to your religious beliefs. You agree to categorise content only under those categories that are relevant to the content. In general, we advise attempts to categorise content under more than five categories will lead to that content being reviewed and possibly removed. You acknowledge that we reserve the right to edit release's tags to ensure your release is sent only to relevant people. By using Get The Word Out, you agree to only publish information that you know to be true and accurate. You are solely responsible for the facts and accuracy of all information submitted by you for distribution by Get The Word Out. InfoChoice lists more than 2,000 financial products from 145 Australian banks, credit unions, building societies and non-bank lenders. With a conventional, non-Sharia mortgage, you’d buy the property with a mortgage agreement that involves funds borrowed from the lender. Islamic Bank In Australia You’d then repay the loan, with interest, over a set repayment period. Islamic finance is based on a belief that money should not have any value itself, with transactions within an Islamic banking system needing to be compliant with shariah . Sharia – compliant loans take roughly the same time to arrange as western-style mortgages. That can involve valuations and a detailed examination of your personal financial circumstances so it’s a good idea to allow a few weeks. The state’s Premier has said residents impacted by this year’s floods will be offered buy-backs and land swaps, however no date has been... The information on this website contains general information only. We have not taken into consideration any of your personal objectives, financial situation or needs. Afiyah helps Australian Muslims get into their dream homes without compromising their beliefs. We provide peace-of-mind and guidance every step of the way by providing Halal Home Loans so you can make better financial choices. It is thus incumbent upon Muslims to find a way of lending, borrowing, and investing without interest. Islam is not the only religious tradition to have raised serious concerns about the ethics of interest, but Muslims have continued to debate the issue with vigour. The head of local Islamic finance company Amanah Finance explains that the core philosophy goes further than avoiding interest. Before the couple met, Melike had also previously taken out a traditional home loan with Commonwealth Bank. How ICFAL gives you the chance to Shariah Compliant investment and financing. Marking 25 years in operation, we are excited to share our brand new visual identity. No, Sharia Loans Australia there is no restriction on non-Muslims taking out Sharia-compliant home loans; however, as there is no financial benefit to non-Muslims, it's not often an option offered to them. The unique circumstances surrounding an Islamic home loan and the limited size of the market can cause lenders to charge more compared to a typical home loan in the form of profit. Murphy stresses that when comparing Islamic home loans, you should keep an eye out for the service level offered by the provider. As the Islamic religion forbids borrowing money to be repaid with interest, Aaban approaches a local financial institution that provides alternative forms of lending. The lender conducts a preliminary assessment of Aaban's financial situation and issues a conditional letter of approval on behalf of the funder. They’re invaluable and necessary for Muslim homebuyers because they were designed from the ground up to provide an alternative to mortgages that respect Sharia law and the Islamic belief system. A limitation of Islamic financing is that there are some types of lending products which are Halal Finance not yet available in an Islamic form, such as SMSF lending. Muslim customers will also need to conduct further due diligence when looking for finance products to ensure they are compliant, which may limit their options. This method of Islamic financing differs from a traditional loan in that monies are not simply extended by the financier to the customer for the purchase of an asset, as is the case with a traditional loan. Rather, an asset is purchased by the financier and then sold to the customer. Ribā means that both receiving and paying interest is forbidden. While western mortgages use interest as the primary basis for lenders to make money, Islamic home loans work differently. They operate more like a rent-to-buy agreement, and no interest ever gets charged or paid. To compare and apply for Islamic home loans, contact a Islamic Bank Australia Sharia-compliant financial institution, such asMCCA,ICFAL,Amanah, Hejaz Financial Services, or Iskan Finance. You can also contact other banks to find out if they offer Islamic home loan options. Islamic home loans are different to the mortgages offered by most banks. MCCA Islamic Home Finance Australia Shariah Compliant Halal Finance Muslim mortgage "You have a growing Muslim middle class whose needs need to be addressed by institutions like Crescent Wealth and MCCCA," said Ibn Arabi El Goni, head of product with Dubai-based DinarStandard, which produced the report. A Sharia-compliant home loan means you can move into the property you want and gradually pay it off without compromising your religious principles. The income fund will take 1 percentage point of gross profit and is targeting returns between 3 per cent and 4.45 per cent, while returns on the capital fund will reflect the wider residential market. Crescent Finance’s predictions are based on estimates of financing between 1350 and 1650 homes over the next five years, Dr Farook said. He recently acquired a car, but to avoid buying it through finance, ended up leasing it, which was more expensive and meant he didn’t actually own the vehicle.

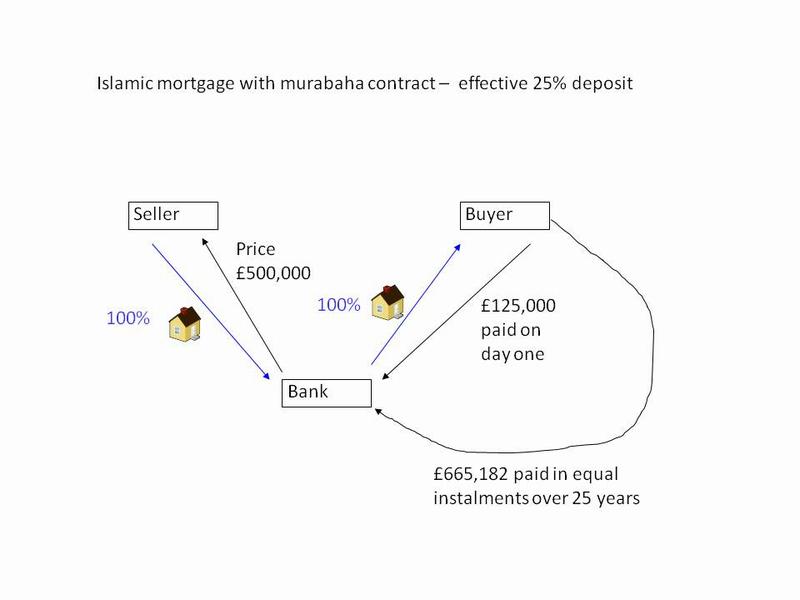

All fees are negotiated with institutions on a case by case basis and may vary between products and providers. Some institutions apply annual account management fees that can bump up the cost of your monthly payments, so look for deals with low or no fees. There’s not a huge number of such products on the market, as the Muslim population of Australia is only around 2.6 per cent, but some of the bigger banks offer loans suitable for Muslims. When considering an Islamic home you will need to think carefully about what you can afford. Different lenders have different rules about the size of deposit they require from you in comparison to the value of the property they will buy. I believe Iskan Finance operates as an ethical business and we’re firm on NCCP compliance so people should take the comfort in the fact that we, and other providers, respect people’s rights under Australian law." None of the Islamic financing companies currently offering consumer finance products in Australia are licensed as fully fledged banks. That means that while they can offer home loans or super, they can't take deposits from customers. And at least two entities are seeking a licence to establish Islamic banks in Australia, alongside non-bank financial institutions that already offer sharia-compliant services. Islam prohibits interest from being charged on home loans. To get started we will conduct an initial pre-assessment to determine how much we can finance you and whether you will fit the requirements for eligibility. The information you provide us here will be verified with supporting documents which we will ask you to provide later. We are rigorous about ensuring the Shariah integrity of our products through Shariah audits and on-going testing. You’d then repay the loan, with interest, over a set repayment period. When you enter into an Islamic home loan agreement, you select your property and your financial institution buys it outright from the seller. Then, the institution agrees to lease the property to you for a set period of time – usually around 25 years – and this is known as Ijarah Muntahiyah Bittamlik. In Islamic banking, charging interest is forbidden under Sharia law, so most home loans won’t be appropriate for Muslims; thankfully there are Sharia-compliant mortgages and products available in Australia. Bear in mind that your choice is not limited to bank based in predominantly Islamic countries. Some of the larger Australian banks also offer Sharia-compliant loans. The major bank has launched a specialised financing product for Islamic business customers. Islamic finance may have just reached a new level, with Sydney company Ijarah Finance now able to offer a suit of lending products previously unmatched in the niche finance market. The key to Islamic banking is interest-free since its bottom line is Islamic compliance. However, in many cases, the banks which are offering interest-based loans are offering Islamic banking as well, which Dr Hassan considers 'conflicting'.

We will order a valuation of the property once you have provided us with a valid contract of sale. Remember, if you change your mind cancelling a sale may become an expensive exercise. Our products have been developed in close collaboration with some of the world’s leading Islamic finance scholars. If you decide to apply for a credit product or loan, you will deal directly with a credit provider, and not with Canstar. Rates and product information should be confirmed with the relevant credit provider. For more information, read the credit provider’s key facts sheet and other applicable loan documentation for that product. This advice is general and has not taken into account your objectives, financial situation, or needs. Are there any Sharia home loans or Islamic banks in Australia? He said Australia's financial industry should follow the lead of the agricultural industry, which he said decades ago made the decision to dominate halal exports. Mr Johnston credited National Australia Bank as being the only major bank to have a specific Islamic-focused financing team. Because the Koran forbids charging interest, financial transactions in the Muslim world have to be structured differently, with assets typically transferred to the financier so they can receive profit instead. But Dr Choudhury said the biggest demand for Islamic finance is for home loans. "In my view, there should not be two types of banking in the same bank, you cannot mix haram and halal," he said. "This variable outweighs religion in terms of importance for patronising types of banking. Therefore, unless people see actual benefits in terms of returns, the extent of patronisation will be nominal." "The difference between Islamic and Western banking is the notion of interest rates," says Nail Aykan, marketing manager with the Muslim Community Cooperative of Australia . "In the Islamic beliefs, the interest rate is forbidden, hence there must be an alternative." This poses a clear difficulty for Muslims in Australia who would want to take out a mortgage while still following Islamic law. Our products have been developed in close collaboration with some

0 Comments

Leave a Reply. |

ArchivesCategories |

RSS Feed

RSS Feed